How Advisors Use the 1040 to Identify Planning Opportunities

For many advisors, the 1040 is something to review during tax season. It’s checked for accuracy, filed away, and rarely referenced again in client conversations.

That’s understandable. Tax preparation usually sits with the client’s CPA, and advisors want to stay within clear boundaries.

But the 1040 isn’t just a tax document. It provides a clear record of what actually happened in a client’s financial life over the past year: income decisions, investment activity, distributions, and timing choices.

Advisors who review the 1040 this way aren’t trying to do tax preparation. They’re using it to understand outcomes and guide better planning conversations.

Reviewing a client’s 1040 can help financial advisors anchor planning conversations in real financial outcomes rather than market headlines.

How reviewing the 1040 changes how clients see you

Without a clear starting point, review meetings can drift.

Markets set the agenda. Headlines drive the questions. Clients walk in reacting to whatever the news cycle delivered that week.

Starting with the 1040 changes that dynamic because it anchors the conversation in the now.

Instead of projections or market commentary, you begin with what actually happened:

- income that showed up

- money that moved

- decisions that played out

There’s no speculation. Both you and the client are looking at the same outcomes.

That simple shift does two things.

First, it gives you control of the meeting. Instead of reacting to market anxiety, you guide the discussion based on real financial activity.

Second, it changes how clients see your role.

Clients expect their CPA to file the return. They don’t expect their advisor to reference it. When you do, it signals that you’re paying attention to the full financial picture, not just the portfolio.

That distinction becomes especially important when markets are uneven. Advisors who rely solely on portfolio performance to demonstrate value are vulnerable in those periods.

But when meetings start with outcomes, the conversation naturally broadens to income planning, distribution timing, and long-term tradeoffs.

Over time, that compounds. Clients stop evaluating you based only on short-term returns and start relying on you to help interpret their financial life as a whole.

Using the 1040 without crossing into tax advice

Advisors often hesitate to use tax returns because they want to stay within clear boundaries.

That caution is reasonable. The 1040 is dense and closely associated with tax advice. It’s easy to worry about contradicting a CPA or getting pulled into technical tax discussions.

But reviewing a return does not mean providing tax advice.

Advisors who use the 1040 effectively focus on understanding outcomes, not fixing the return. They look at what happened last year and what it might mean for planning going forward.

A few guardrails help keep that conversation firmly in planning territory:

- Lead with questions

Ask questions like “Was this intentional?” or “Do we expect this again?” - Focus on patterns

Look for trends in income, investment activity, or distributions rather than prescribing strategies. - Keep the scope narrow

One or two meaningful observations are usually enough to move the conversation forward. - Collaborate with the CPA

If something requires deeper tax analysis, bring the CPA into the discussion.

Used this way, reviewing the 1040 strengthens planning conversations without stepping outside an advisor’s role.

Many advisors want to do more around taxes but hesitate because of compliance boundaries. In this on-demand recording, tax expert Steven Jarvis, CPA, explains how advisors can identify real planning opportunities, set clear expectations with clients, and have smarter tax conversations without stepping outside their role. Click here to watch the recording.

A simple framework for reviewing the 1040

Using the 1040 effectively does not require a detailed tax analysis. The goal is simply to identify signals that matter for planning.

A quick, consistent scan is usually enough.

- Start with what changed

Look at total income and adjusted gross income. If those numbers moved meaningfully, something happened that deserves a conversation. - Scan for unexpected activity

Look for income sources or investment activity that don’t match how the client describes their situation. Small streams, unexpected gains, or strategy drift often show up here. - Flag distributions and one-time events

Retirement withdrawals, liquidity events, or income spikes usually reveal timing decisions or cash-flow needs. - Ask questions instead of prescribing solutions

The goal isn’t to solve everything in the meeting. It’s to understand what happened and what may matter going forward.

Used this way, the 1040 becomes a quick orientation tool rather than a detailed tax review.

Turning the 1040 into a planning advantage

By the time a client sits down for a review meeting, most of the year’s meaningful financial decisions have already happened. The 1040 captures those decisions in one place, which is why it can anchor better planning conversations.

The challenge for many advisors isn’t understanding the tax return. It’s reviewing it consistently and translating what they see into productive client discussions.

That’s where structure helps.

Tools like the Advisor’s Tax Season Operating Checklist give advisors a repeatable workflow for tax season, from early planning through post-filing reviews.

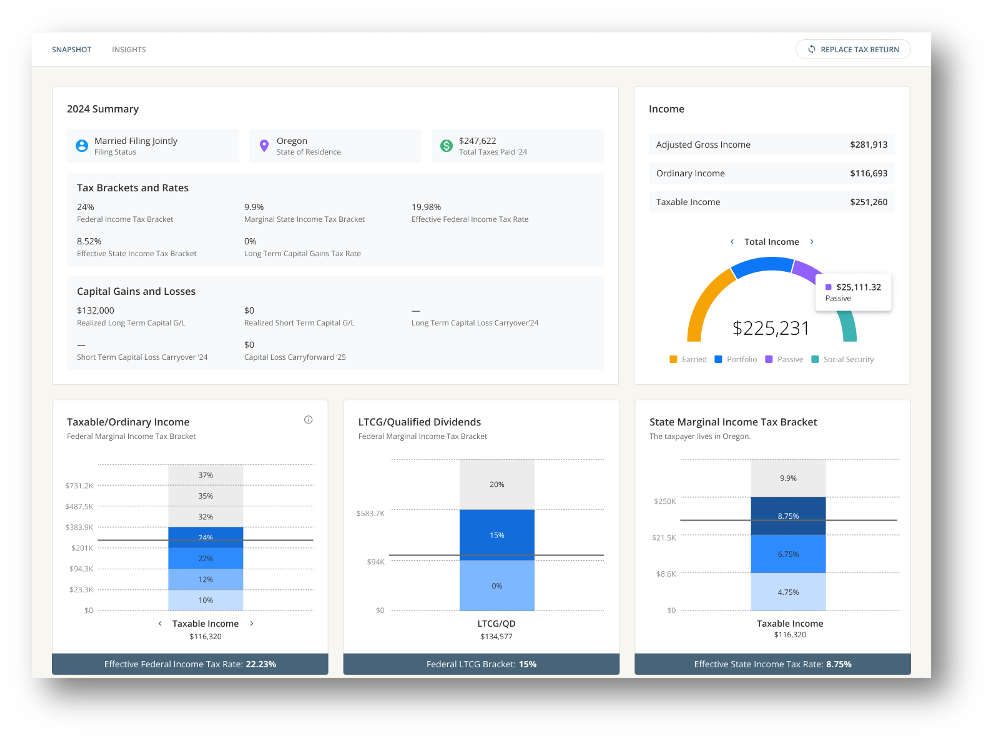

And when you want to quickly turn a tax return into something clients can understand, Nitrogen’s Tax Center can help generate a visual tax snapshot in minutes. It surfaces key insights from the return and turns them into a clear starting point for planning conversations.

Used together, these tools help advisors review returns faster, identify potential planning opportunities, and lead more focused client meetings during the busiest stretch of the year.

Frequently Asked Questions (FAQs)

What is the 1040 form?

The 1040 is the primary federal income tax return used by individuals in the United States. It summarizes income, deductions, credits, taxes owed, and major financial activity for the year. \While it summarizes taxes owed, it also provides a consolidated, backward-looking view of a client’s actual financial behavior.

Why should financial advisors review a client’s 1040?

Because the 1040 reveals what account statements often hide. It helps you anchor conversations in reality, showing exactly where income was earned, when money moved, and which tradeoffs were made. It also helps you uncover hidden accounts and held-away assets (like high cash balances in Schedule B) that a client may have forgotten to mention.

Is reviewing a tax return the same as giving tax advice?

No. There is a clear line between “tax preparation” and “tax-aware planning.” Reviewing a 1040 to identify patterns, Medicare thresholds, or Roth conversion opportunities is a planning service. It allows you to ask smarter questions and coordinate more effectively with the client’s CPA without stepping outside your professional boundaries.

What should advisors look for on a 1040?

Advisors typically focus on changes in income, unusual or recurring income sources, distributions, large one-time events, and activity that does not align with the client’s stated plan. Advisors can also spot opportunities in Roth conversions, deductions, and capital gains, along with undisclosed cash or held-away assets.

How does this improve client meetings?

It shifts the meeting from defending the portfolio to guiding the household. By starting with a visual Tax Snapshot of what actually happened, you establish a shared reality. This builds instant credibility, broadens the conversation beyond market returns, and justifies your value through comprehensive, tax-aware guidance.

Can advisors use a 1040 review for prospecting?

Absolutely. Offering a Tax Snapshot is a low-friction, high-value way to start a relationship. It allows you to lead with a breakthrough insight rather than a sales pitch. Showing a prospect insights they may not have previously discussed with an advisor, like a missed deduction or a hidden account, is one of the most effective ways to convert them into a client.

How does this fit with a client’s CPA relationship?

Reviewing the 1040 can strengthen collaboration. Advisors use it to understand outcomes and planning implications, while CPAs remain responsible for tax preparation and technical tax advice. When questions arise, involving the CPA helps maintain clear roles.

How can advisors review the 1040 efficiently?

Many advisors use structured checklists or tools, such as Nitrogen’s Tax Season Operating Checklist or Tax Center, to quickly surface relevant planning signals without performing a full tax analysis.