The Most Overlooked Way Advisors Demonstrate Their Value

Why tax-aware planning conversations create the biggest “aha” moments for clients.

Many advisors have experienced a moment like this in a client meeting.

You’re reviewing the portfolio and discussing long-term strategy. The client nods along politely.

Then a tax question comes up.

Maybe it’s about selling an investment. Or harvesting losses. Or which account to withdraw from in retirement.

You walk through the implications.

The client pauses.

“Wait… I didn’t realize that mattered.”

And suddenly the tone of the meeting changes.

Moments like these often become some of the clearest demonstrations of an advisor’s value. And they frequently happen during tax-aware planning conversations.

Why Advisor Value Can Feel Invisible

Advisors spend much of their time doing work clients rarely see.

Designing portfolios, managing risk, and adjusting strategies are essential parts of long-term financial planning. Yet their impact often unfolds gradually. In a single client meeting, the value of those decisions can feel abstract.

This creates a challenge for many advisors.

The most important parts of their work do not always produce a clear moment when clients recognize the value being delivered.

But certain conversations change that dynamic.

When tax implications enter the discussion, financial advice becomes more tangible. A decision about selling an investment or structuring withdrawals can immediately affect what a client keeps after taxes.

In those moments, the value of planning becomes easier to see.

Clients begin to recognize how financial decisions connect across investments, income, and long-term strategy. And they begin to see the advisor as the professional helping them navigate those connections.

How Tax Conversations Shift Client Perception

Many financial planning conversations begin with investments. Portfolio performance, market conditions, and long-term strategy tend to dominate the discussion.

Taxes, on the other hand, are often treated as a separate conversation. Clients assume their accountant is handling them, and advisors sometimes hesitate to step too far into what feels like another professional’s territory.

As a result, tax implications can remain in the background of financial planning discussions. The advisor’s work can appear narrowly focused on investments, even when their planning process is much broader.

But when taxes do enter the conversation, something often changes.

A client might realize that selling an investment this year could push them into a higher tax bracket.

Or that harvesting losses in one part of the portfolio could offset gains elsewhere.

Or that withdrawing from one account instead of another could change how much retirement income they keep.

That’s often when the meeting pauses.

Clients lean forward.

“Wait… I didn’t realize that mattered.”

“So if we do this now, it changes the taxes I pay this year?”

Moments like that often open the door to another kind of discovery.

When advisors begin looking more closely at a client’s tax situation, they frequently uncover details that never surfaced in earlier conversations. A quick review of a document like a 1040 can reveal income sources or accounts the advisor didn’t previously know about.

- Interest income from an unfamiliar bank.

- Dividend payments from a brokerage account held elsewhere.

- Capital gains activity from investments outside the client’s current strategy.

Each line item raises a simple question.

“Tell me about this account.”

Sometimes the answer leads to an old brokerage account that was never incorporated into the plan. Other times it reveals a legacy portfolio, a large cash balance, or an investment relationship the advisor didn’t realize existed.

Moments like these don’t just clarify tax implications. They often reveal parts of the client’s financial life that had been operating quietly outside the broader plan.

The Line Advisors Worry About Crossing

Of course, tax conversations can also create hesitation for advisors.

Many are careful about stepping into territory that traditionally belongs to accountants or tax preparers. Compliance expectations, liability concerns, and professional boundaries all play a role. No advisor wants to give the impression they’re providing formal tax advice.

That hesitation is understandable.

But there’s an important distinction between tax advice and tax-aware financial planning.

Advisors aren’t responsible for interpreting every detail of the tax code or preparing a client’s return. Instead, their role is often to help clients understand how financial decisions interact with taxes.

Advisors who incorporate tax awareness into planning conversations often follow a few simple guardrails:

- Start with questions. Rather than prescribing tax strategies, advisors focus on understanding what happened and whether similar situations might occur again.

- Focus on planning implications. The goal isn’t to fix last year’s tax return. It’s to understand how financial decisions may affect future outcomes.

- Collaborate with the client’s CPA. If a situation requires deeper tax analysis, bringing the client’s accountant into the conversation keeps everyone aligned.

Approached this way, tax awareness stays firmly within an advisor’s role. It becomes another way to help clients make more informed financial decisions.

The Two “aha” Moments for Clients

In many cases, tax-aware planning conversations create two important “aha” moments for clients.

First, tax insights provide a tangible demonstration of the advisor’s value.

Instead of discussing abstract planning concepts, the advisor is pointing to decisions that have clear financial consequences. Clients can immediately see how thoughtful planning affects what they ultimately keep after taxes.

Second, clients begin to see their advisors in a broader role.

The conversation is no longer just about investments or market performance. It becomes clear that the advisor is helping them think through how financial decisions connect across taxes, income, and long-term planning.

Once those connections become visible, the client’s perception of the advisor often expands.

Financial decisions that might once have happened independently start coming back to the advisor for input. Clients ask about the tax impact of selling a property, exercising stock options, or structuring retirement withdrawals.

Instead of turning to their advisor only for portfolio updates, they begin to see them as someone who helps guide the broader financial decisions shaping their future.

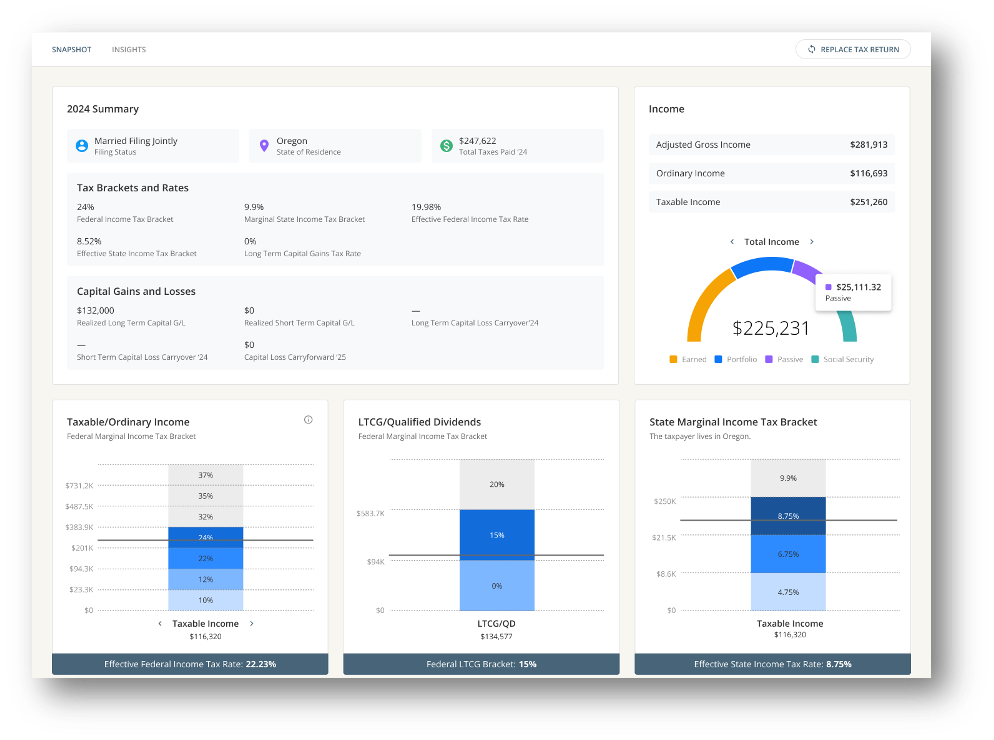

Nitrogen’s Tax Center turns any 1040 into clear visuals, making complex tax data easy to understand.

Nitrogen’s Tax Center turns any 1040 into clear visuals, making complex tax data easy to understand.

Why That Shift Matters for Advisors

What begins as a simple conversation about taxes can often lead to something much more valuable: deeper client relationships and a stronger advisory practice.

When clients begin to see their advisor as someone coordinating their broader financial life, the relationship often evolves in ways that directly benefit the practice:

- Discovery and consolidation of held-away assets. Tax documents often reveal accounts or investments the advisor didn’t previously know about. Once those assets come into view, clients frequently ask whether they should be incorporated into the broader strategy.

- Greater share of the client relationship. As advisors become involved in more financial decisions, they naturally become responsible for a larger portion of the client’s financial life.

- Stronger client retention. Clients who rely on their advisor for a broader range of decisions are far less likely to look elsewhere for advice.

- More referral opportunities. When clients see their advisor as a trusted financial guide, they are more likely to introduce them to friends, family members, or colleagues facing similar questions.

In many cases, the path to deeper client relationships can begin with something as simple as a conversation about taxes.

Turning Insight Into Conversation

Many advisors have already seen how powerful tax conversations can be in client meetings. A well-timed insight about capital gains, withdrawal timing, or income strategy can quickly turn an abstract planning discussion into something tangible.

But those conversations don’t have to stop at the desk.

Tax awareness can also create opportunities to educate clients, spark new discussions, and connect with investors who may not yet have an advisor helping them think through those decisions.

Because often the best way to demonstrate the value of advice is to start with the questions investors are already asking.

Frequently asked questions about tax-aware financial planning

Why should financial advisors discuss tax considerations with clients?

Tax considerations often influence how financial decisions play out in real life. Investment sales, retirement withdrawals, and income timing can all affect what clients ultimately keep after taxes. When advisors incorporate tax awareness into planning conversations, they help clients understand how different decisions interact across investments, income, and long-term financial goals. These conversations can also reveal planning opportunities that might otherwise go unnoticed.

Are financial advisors allowed to give tax advice?

Financial advisors typically do not prepare tax returns or provide formal tax advice. However, many advisors incorporate tax awareness into financial planning discussions. This means helping clients understand how investment decisions, withdrawal strategies, or income timing may have tax implications. Advisors often collaborate with a client’s CPA or tax professional to ensure financial decisions align with the client’s broader tax strategy.

How can tax conversations strengthen the advisor–client relationship?

Tax conversations often help clients see how different parts of their financial life connect. When advisors highlight how investments, income decisions, and taxes interact, clients gain a clearer understanding of their financial plan. These discussions can shift the advisor’s role from someone who manages investments to someone who helps guide broader financial decisions, which often strengthens trust and engagement.

What can financial advisors learn from reviewing a client’s tax return?

A client’s tax return can reveal valuable information about their financial situation. Interest income, dividend payments, capital gains, or deductions may indicate accounts, income sources, or investment activity that were not previously discussed. Reviewing these details can help advisors identify planning opportunities and ensure the client’s financial decisions are aligned with their broader strategy.

How can tax-aware conversations help advisors grow their practice?

When advisors incorporate tax awareness into financial planning discussions, they often gain deeper visibility into their clients’ financial lives. These conversations may uncover additional assets, financial decisions, or planning needs that were previously outside the advisor’s scope. Over time, this can lead to broader planning relationships, stronger client retention, and opportunities to consolidate assets into a more coordinated strategy.