5 Ways to Start Estate Planning Conversations With Clients

Estate planning conversations are easy to put off. Clients may assume there’s plenty of time, avoid uncomfortable topics, or believe their family already knows what to do. Advisors have their own hesitations too, especially when timing feels off or the topic feels heavy.

But waiting has a cost.

As the Great Wealth Transfer continues, advisors who’ve already built relationships with families are in a very different position than those meeting beneficiaries for the first time mid-transition.

The challenge is finding a natural way in.

In many cases, the best opening has little to do with estate documents themselves. A marriage, a new child, aging parents, or a major financial change often creates a more comfortable entry point for conversations about family communication, decision-making, and long-term preparedness.

Below are five moments when estate planning conversations tend to feel timely rather than intrusive.

1. Marriage or partnership changes

Marriage, remarriage, and long-term partnership changes often force clients to revisit financial decisions they may not have reviewed in years.

A growing household can quickly raise important questions:

- Who should be listed as a beneficiary?

- How should assets be titled?

- Are there children from a previous relationship to consider?

- Would each partner know how to access important financial information if something happened unexpectedly?

Advisors don’t need to begin with estate documents or legal terminology. In many cases, a broader conversation feels more natural:

“Now that your household has changed, let’s make sure your financial plan reflects the people you want to protect.”

Clients often focus less on paperwork and more on whether the right people are prepared and informed.

2. The birth or adoption of a child

Few life events reset a client’s planning priorities faster than welcoming a child.

Clients who once viewed estate planning as a future problem suddenly start asking bigger questions about protection, responsibility, and preparedness. They may want to revisit beneficiaries, guardianship decisions, insurance coverage, and whether their family would know what to do during an unexpected situation.

Advisors don’t need to frame the conversation around worst-case scenarios. In many cases, preparedness is the more effective starting point:

“Now that your family has grown, let’s make sure the people who depend on you are reflected in your plan.”

Advisors can also move the conversation beyond documents alone. Who understands the family’s financial picture? Who would know who to call? Who could help coordinate decisions during a stressful moment?

Those conversations often uncover planning gaps clients hadn’t considered and help families feel more prepared for the future.

3. Aging parents or caregiving responsibilities

Many clients begin thinking differently about their own estate planning when they’re helping aging parents through a transition.

They see firsthand how difficult it can be to locate accounts, understand a parent’s wishes, coordinate siblings, or contact financial professionals during a stressful period. They may also see the difference between a family that prepared early and one trying to make important decisions with limited information.

For advisors, these moments often create a more natural opening for estate planning conversations.

A client helping care for a parent may begin asking difficult questions of their own:

- Are my affairs organized?

- Would my children know what to do?

- Would my family know where to find important information?

Advisors can use this moment to help clients turn a difficult family experience into a more thoughtful plan for their own household. The conversation can focus less on legal documents and more on helping families reduce confusion, improve communication, and prepare the right people before a transition occurs.

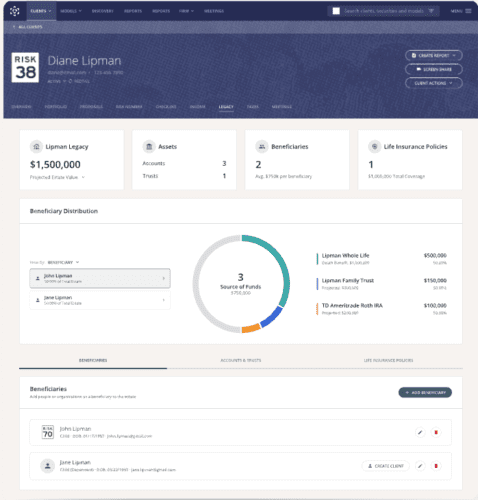

Tools like Legacy Center help advisors make that preparation visible by giving clients a clearer picture of how their estate is organized and helping them build intentional connections with beneficiaries before wealth changes hands.

Estate plans are easier to discuss when clients can actually see them.

4. Divorce, inheritance, or a major liquidity event

Some financial transitions surface planning decisions clients haven’t revisited in years.

A divorce can change who a client trusts to make decisions or inherit assets. An inheritance may introduce new family expectations and financial responsibilities. A business sale or major liquidity event can move priorities from building wealth to preserving it and preparing to pass it on.

Clients often begin reconsidering who should be included in their plan and how they want future decisions handled.

Advisors can help clients pause and make sure their financial plan still reflects their current life.

A simple prompt can open the door:

“Since your financial picture has changed, it’s worth revisiting who’s included in your plan and whether your current instructions still reflect your wishes.”

Clients are more receptive when the conversation connects to something real happening in their life right now.

5. Retirement and legacy planning

Retirement tends to shift planning conversations toward family, legacy, and how clients want their wealth to support others.

Clients may begin thinking more seriously about supporting children or grandchildren, giving to causes they care about, simplifying finances, or preparing a spouse to manage important decisions.

Retirement conversations often open the door to family preparedness discussions.

Many clients have an estate plan on paper, but their family may not know who the advisor is, where key information lives, or what conversations have already happened. Advisors can help clients prepare the next generation before a transition occurs.

Advisors can help clients think through which conversations matter most and how much detail to share with the people who need it.

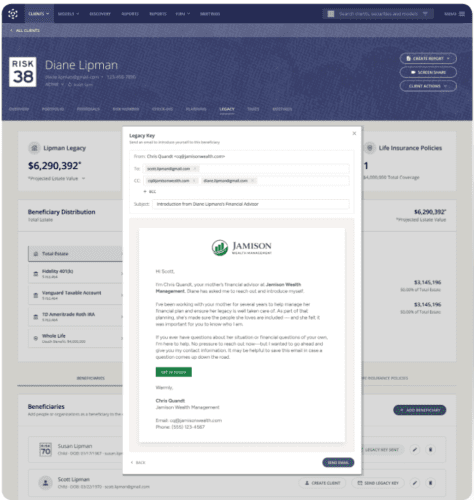

Legacy Key helps turn estate plans into clearer family communication.

Make estate planning a part of the client relationship

The advisors who navigate the Great Wealth Transfer most effectively likely won’t be the ones meeting beneficiaries for the first time after wealth changes hands. They’ll be the ones building family relationships long before a transition occurs.

The earlier advisors involve families, the easier major transitions become.

Estate planning conversations create opportunities to involve the next generation earlier and reduce confusion during major life changes. Tools like Nitrogen’s Legacy Center help advisors make those conversations easier to navigate and help families understand how assets may transfer over time.

Interested in learning more? Book a demo to learn more about Legacy Center and the rest of the Nitrogen platform.

Frequently Asked Questions

What is Legacy Center?

Legacy Center helps advisors build intentional relationships with clients’ beneficiaries before a wealth transfer occurs. Advisors can use Legacy Center to generate a Legacy Map, which creates a visual picture of a client’s projected estate including accounts, trusts, insurance policies, and beneficiaries tied to projected dollar amounts.

What does a Legacy Map show?

A Legacy Map is a visual projection of a client’s estate based on their current accounts, income plan, and beneficiary designations. It shows beneficiaries, including children, trusts, organizations, and other parties, alongside projected dollar amounts in real future dollars. Because Legacy Center pulls from data already in Nitrogen, setup is fast and the projections are grounded in the client’s actual financial plan.

What is a Legacy Key?

A Legacy Key is a formal, advisor-branded introduction that can be sent to a client’s beneficiaries through Nitrogen with the client’s permission. It gives beneficiaries the right contact information and a clear reason to connect with the advisor when the time comes.

When should advisors bring up estate planning with younger clients?

Advisors should bring up estate planning when a younger client experiences a major life change, such as marriage, having a child, buying a home, receiving an inheritance, or starting a business. Age alone shouldn’t determine when the conversation begins.

Does Legacy Center replace estate planning software?

No. Legacy Center isn’t designed to help advisors draft or execute estate documents. Legacy Center focuses on the relationship side, helping advisors build intentional connections with beneficiaries and giving clients a visual picture of how their estate is likely to flow, so the next generation knows who to call when the time comes.

How does Legacy Center help with next-gen client retention?

When a client passes, assets often leave with the beneficiaries, because beneficiaries tend to choose advisors they already know. Legacy Center helps advisors build that familiarity before a transition occurs, by giving clients a natural way to introduce their advisor to family members while they’re still in the room. The Legacy Key creates a formal, lasting connection that doesn’t depend on a business card in a drawer.

What is the Great Wealth Transfer?

The Great Wealth Transfer refers to the estimated $84 trillion in assets expected to pass from Baby Boomers and older generations to their heirs over the next two decades. It’s considered one of the largest intergenerational wealth movements in history, and it has significant implications for financial advisors whose clients are approaching or in retirement.

How do financial advisors engage the next generation of clients?

The most natural approach is through an existing client relationship. When advisors help clients think through who their beneficiaries are and how wealth will transfer, it creates a legitimate, client-approved reason to connect with the next generation, before a transition occurs. Cold outreach to a client’s children rarely works; a warm introduction from the client themselves is a different conversation entirely.