Investment Team

Continue reading “Why Nitrogen Advisors Use Retirement Maps In Every Meeting”

Continue reading “Why Nitrogen Advisors Use Retirement Maps In Every Meeting”

Will the rule be overturned?

Will the rule be postponed so they can add some color to it?

Does President Trump even know what he signed last week?

The latest news stems from an executive order Trump signed on Friday, February 3rd, which was rumored to delay the fiduciary rule until the Republicans could kill it. There are differing opinions about what’s actually happening, but it appears that the rule hasn’t expressly been delayed quite yet.

One take is that the rule won’t be overturned because large industry players have already made sizeable investments in preparation for it.

For example:

Merrill Lynch eliminates commission IRA business in response to DOL rule

Ameriprise spends $11 million-plus this year on DOL fiduciary rule

This is certainly an indication that it will be hard to fully walk the DOL ruling back to the starting line.

But for now, the DOL rule’s applicability date remains: April 10, 2017. Could that change? Maybe. What do I think?

I actually don’t think it matters.

The Best Interest Economy is here to stay.

Why? Because after all the education that the Department of Labor, industry associations and firms themselves have done for the public, I can’t see clients accepting a return to not acting in their best interests.

So what are the central tenets of the Best Interest Economy? It has three core pillars.

In the Best Interest Economy, advisors will have to disclose fees to an indisputable degree of clarity, and fees must be “reasonable.”

The most interesting aspect of this discussion is that few are arguing that a 1% advisory fee is unreasonable. The focus has been on products that charge 5%, 6%, 7% commissions. Fee benchmarking tools will further drive this kind of clarity around what a “fair” cost of advice is.

But the real change in fees comes from the asset management side. The days of the 300+ basis point managed account programs are numbered, especially when that eats up 50-60% of the client’s average returns. ETF providers are leading the way with internal expenses going to single digits in the most extreme cases.

Where our industry delivers value, fees will continue to be justified, and it’s clear that real advisors who help their clients make great decisions, plan for the future and navigate complexity deliver value. That kind of advisor can continue to make healthy margins by adding scale and efficiency to their businesses.

Clients are already putting a lot of pressure on advisors to up their technology game. They want a wealth management experience like they get from their credit card company, their bank…and pretty much every other critical part of their lives. When clients have to transport themselves back to the nineties to check on their wealth, that’s clearly a problem.

The good news is that this is changing. Advisors are investing in technology. The onus is now on the technology companies to deliver excellent client-facing experiences so that all the spending doesn’t go to waste.

Here’s the best news: this is the solution to fee compression, and your clients are presenting it to you on a silver platter. An advisor’s most valuable asset is their time. The advisor is the product, and they only have so many hours to spend with clients. By delivering better client experiences and focusing their time where they actually deliver value, advisors gain substantial scale and efficiency, letting them bring on more clients while minimizing overhead. This is an advisor’s best weapon against fee compression.

I’ve heard the term “data is the new oil” countless times in the past five years. To put it another way, decisions without data are becoming a thing of the past.

Facebook won’t make a decision to change their algorithm or news feed without substantial testing data to back that decision up.

Employees that present data-less solutions at Uber’s corporate offices are asked to leave the room until they can return with numbers to support critical decisions.

Today, data has never been more accessible, and we have oceans of data to draw from to determine who our best clients are, how much risk they can handle, how to align them with the right amount of risk, and how to help them reach their goals.

How will you be able to prove that you are acting in a client’s best interests if you do not have the quantitative data to back it up?

Advisors that succeed in the Best Interest Economy will use a quantitative approach, not a subjective one.

No matter what happens to the DOL fiduciary rule, the three pillars of the best interest economy are here to stay. Be prepared.

Want to keep preparing for the Best Interest Economy? Here’s a download link to a checklist we’ve put together: Can a Fiduciary Manage 100+ Clients?

This post was revised February 6th, 2017 at 10:30am PST to reflect current events surrounding the Department of Labor.

We pride ourselves in our respect for the markets. We believe that price is truth and that you need to approach investment analysis with humility or you risk being humbled by the complexity of the markets.

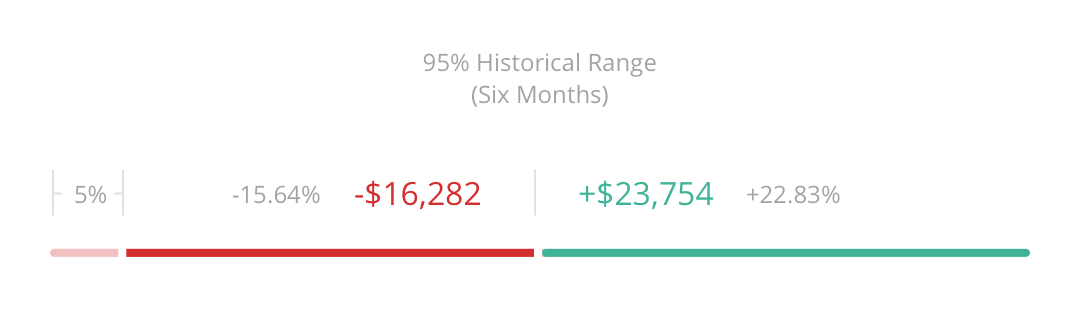

Our Risk Number’s corresponding six-month, 95% Historical Range is a historical calculation using a variety of statistical inputs, based on the price history (expense ratios, dividends, etc.) at the holding level. This bears repeating; we do not use the antique process of mapping holdings to a set of assumptions at an asset allocation level. Price, at the holding level, is truth. We derive our statistics from each holding’s actual price history because it is more robust than an asset allocation mapping methodology.

Even though our six-month, 95% Historical Range is a historical calculation that doesn’t explicitly say “here’s what is predicted to happen in the next six months,” we assume that humans may implicitly apply historical probabilities into the future. Even though we can all recite the phrase “Past Performance Is No Guarantee of Future Results,” we test our methodologies to inform best practices for those who implicitly use the past as an input for what to expect in the future.

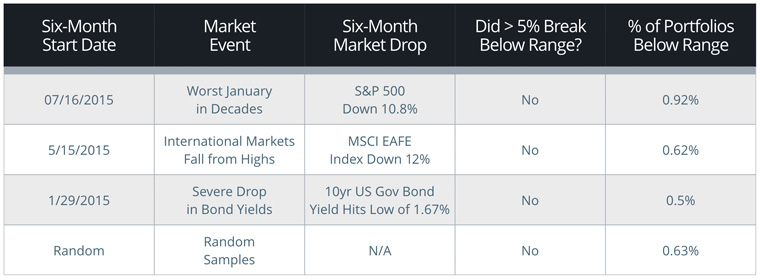

Recently (Fall 2016), we tasked our incredible team of engineers with a project that first required them to identify portfolios that broke below Nitrogen’s six-month, 95% Historical Range in the six months following the calculation. This was a thought exercise to inform best practices and potentially uncover areas for improvement in our methodology.

Random samples failed to produce significant examples of portfolios breaking below the historical range in the six months following historical calculation. In a search for rogue securities and portfolios, we decided to put our methodology through the proverbial ringer by hand-picking a myriad of difficult six-month epochs from the past couple of years. We hand-selected a variety of ranges where the markets jolted downward and were very pleased with the results.

We define a “portfolio” as an account or set of multiple accounts that contain at least two securities. We analyzed over 100,000 unique portfolios (see “Random Samples” above) and saw an average of 0.63% break below the projected six-month, 95% Historical Range; well within expectations.

This data set is focused primarily on 2014-Nov 2016 when markets overall (except in instances like those cited above) have been in a relatively low volatility state.

The six-month, 95% Historical Range is profound because humans make decisions in the short term. Great advisors couple the realities of short-term investor psychology with a discussion of long-term risk capacity (powered by Retirement Maps) to empower their clients to invest fearlessly for the long haul.

by Aaron Klein, CEO

Human nature is against us. Advisors are no strangers to the idea that investors naturally have a tendency to buy when things are good, sell when they get scared, miss the recovery, buy back in when the markets “feel safe again,” and repeat until broke!

In an ongoing attempt to combat this, the financial industry has evolved significantly over the past several decades. The trends we’ve witnessed can be categorized into what I call the three waves of advice.

With so many options, what incentive does an investor have to choose one broker over the other? It all came down to the broker’s promises, of course.

“My mutual fund is way better than that guy’s mutual fund.”

The first wave of advice died abruptly with the discovery of an unfortunate fact: His mutual fund actually wasn’t better than that guy’s mutual fund.

“Let me distract you by talking about your long-term goals.”

Now, before I’m flooded with angry emails about my thoughts on the second wave, let’s get something straight – it’s wise to consider the long term. No decent advisor today would undervalue the ultimate future of a client’s financial health.

The issue here isn’t that we focused on the long-term, the issue is what got ignored. Many advisors began disregarding human nature altogether. This works about as well as your doctor saying “If you exercise now, you’ll thank yourself in 30 years.”

The pendulum’s overcorrection caused many advisors to begin ignoring returns completely. We began ignoring risk, ignoring human psychology, and focusing only on the long term. The problem is, this simply doesn’t work.

All of our research points to a simple truth: while investors should be focused on the long term, they react to risk in the short term, and emotional reactions to risk are the number one killers of long-term financial goals and results.

“How far can a portfolio fall, within a fixed period of time, before the investor will capitulate and make an emotionally-charged, poor investing decision?”

We’re witnessing the third wave of advice: putting risk first. When advisors quantify risk alignment from the start, they set clear expectations for investors. A clear understanding of risk and returns can allow investors to give themselves permission to “hang in there,” even if markets are volatile.

The third wave of advice is catching on more quickly than we could’ve ever imagined. We’re seeing it firsthand. When you quantify risk for an investor, you can empower anyone to invest fearlessly.

Aaron Klein is CEO at Nitrogen, the company that invented the Risk Number and empowers advisors to align clients with their portfolios and expectations.

It’s here. The Department of Labor’s (DOL) fiduciary rule has been finalized, and its intents are clear: “This broad regulatory package aims to require advisers and their firms to give advice that is in the best interest of their customers…” (81 CFR 20947). Advisors must now provide evidence that their advice is “…based on the investment objectives, risk tolerance, financial circumstances, and needs of the Retirement Investor.” (81 CFR 21007). In other words, advisors need to demonstrate and document that their advice is in concert with the amount of risk their clients want, can handle and need.

We started Nitrogen just a couple hours from the Port of San Francisco, which has always been known for two things: a constant flow of international cargo ships, and challenges caused by the dense, Bay Area fog.

Over a century ago, a series of prominent “leading lights” were installed to guide ships through the narrow passageway now marked by the Golden Gate Bridge. Sailors would approach the bay by keeping a few key lights constantly aligned. These lights provided a clear path for steering the ship to what would otherwise have been a disoriented crew.

As we approach the implementation date of the new fiduciary rule, advisors will be able to use risk alignment in the same way. The marvelous thing about quantifying risk for investors is that certain metrics can act as “leading lights” toward an indisputable arrival at a client’s best interest.

There are three measurements of client risk an advisor must quantify in order to exhibit the best interest standard. If these three lights align, an advisor’s client is irrefutably invested correctly.

Yes, that’s right, measure it. The old-school way of stereotyping investors based on their age simply isn’t working. Many Millennials don’t want to be invested aggressively. Many Baby-boomers are well prepared for retirement and don’t want to be stuck in the slow, conservative portfolio. Even if it were that easy, what do those words even mean? A moderately conservative investor looks different to you than it does to me.

Use a reputable tool and quantify how much downside risk your clients and prospects can stomach. You can’t operate in anyone’s best interest without knowing them beyond their outward appearance.

The amount of risk an investor wants is not always the amount of risk an investor needs in order to reach their goals. Operating in a client’s best interest goes beyond investing them in the way they feel is right.

If an investor wants more risk than they need, that could be okay. Documenting both measurements will allow you to guide them toward the best investing decisions. If an investor needs more risk than they want in order to reach their retirement goals, this will frame a different conversation. An advisor can paint the picture that one simply can’t get from San Francisco to New York in less than a day if they’re afraid to fly. Or worse, don’t have enough time for that kind of trip even if flying! Advisors need the tools to be able to explain why the client’s risk, retirement age or savings goals need to change — before the client invests, not after they’re in trouble.

It’s incredible how often I see advisors bring prospects into their office and find alignment in the first two measures of risk, only to discover that they’re currently invested far outside of their risk tolerance.

One advisor just told me a story about a prospect named Greg. Greg sought out this advisor in 2013 when the markets were booming. Greg called him and said, “I’ve been a bit nervous. I like my current advisor, I know him well and golf with him often, but my portfolio has been bouncing around quite a bit. I’ve got $2M and I just feel like I have no margin for error.” Naturally, the advisor sits up in his chair and gets pretty excited… until Greg starts to backpedal. “But, you know, I’ve been making tons of money recently, so I’m not ready to make any changes. Let’s just get to know each other and maybe I’ll hire a second advisor one day.”

The advisor scheduled a meeting with Greg and had a conversation about risk. As it turns out, Greg’s measurable risk tolerance was relatively low. Greg also didn’t need to take on an unreasonable amount of risk in order to reach his retirement goals. Then, these two discovered a game-changer: Greg was invested into a very high-risk portfolio.

Needless to say, when Greg saw the potential downside risk of his current portfolio, he turned white in the face and signed the account transfer paperwork immediately. His advisor may have been a great golf partner, but he certainly wasn’t acting in Greg’s best interest.

Greg’s new advisor fulfilled the DOL’s core mandate by documenting alignment between the three measurements of client risk. Advisors who do the same can navigate any amount of fog brought in by the changing landscape of fiduciary compliance.

Aaron Klein is CEO at Nitrogen, the company that invented the Risk Number and empowers advisors to align clients with their portfolios and expectations.

We’re excited to announce that starting today, advisors now have an even greater set of choices for deciding which market risk assumptions to use when driving the Risk Number® and 95% Historical Range analytics for portfolios.

This calculates the Six Month Historical Range based strictly on average return data, and does not incorporate capital market assumptions. This will allow Nitrogen to more closely match other portfolio analysis tools that use average annual returns.

Continue reading “Giving Advisors More Choices on the Risk Model Driving the Risk Number”

Nitrogen’s newest tools, Check-ins and Client Analytics, are available as a free upgrade to every Nitrogen advisor.

Client Analytics help the advisor put markets, portfolios and risk in context for clients during semi-annual client reviews.

Monthly Check-ins build a strong foundation to support the advisor’s message between client reviews and give advisors an early warning signal when client psychology is deteriorating.

These powerful new tools revolutionize the ability of advisors to put the markets in context for their clients during client reviews, support client psychology between those reviews, and deliver consistent behavioral coaching that promotes long-term investing. The constant fight by advisors to keep client psychology positive just became remarkably easier.

Advisors have used Nitrogen for a long time to effectively set risk expectations for client portfolios, but with Client Analytics, the conversation shifts to demonstrating how well the Risk Number was able to meet those expectations and compare the outcome to the advisor’s choice of benchmark. The result is a powerful way to give the client context for why market volatility is “normal” and help clients stay the course when they may be concerned and prone to knee-jerk reactions.

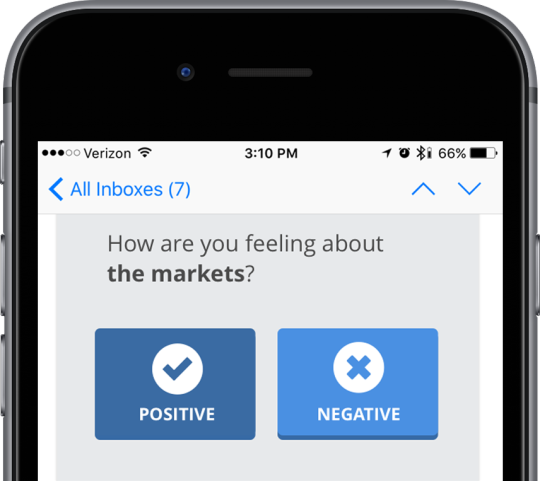

Advisors can leverage a powerful ally in supporting client psychology in between those reviews by enabling Check-ins, a monthly email that gathers two simple data points from each client, and proactively supports the advisor’s message with adaptive analytics that fit the context of the markets.

Two simple questions mark each client’s check-in — “how are you feeling about the markets?” and “how are you feeling about your financial future?” With two taps on their smartphone, clients see adaptive analytics that help them understand what is “normal” for their portfolio, and advisors get an early warning system when a client relationship needs care.

So, what are we waiting for? Check-ins can be enabled now by selecting “show clients” in your Nitrogen dashboard. While you’re at it, view the Check-ins knowledge base article.

The Department of Labor released its much-anticipated fiduciary rule earlier this month, and the Nitrogen team has been hard at work to bring solutions and resources to advisors. See our full press release below and download our white paper at the new dol.riskalyze.com.

Nitrogen Launches Comprehensive DOL Compliance Solutions for Advisors

• Nitrogen stitches together its product line to offer specific solutions for advisors and firms in light of the Department of Labor’s (DOL) fiduciary rule.

• Nitrogen launches dol.riskalyze.com to showcase its unified compliance solution and a free white paper titled “No Need to Panic: A Roadmap to the DOL’s Final Fiduciary Rule and What It Means for Firms and Advisors.”

SACRAMENTO, CA–(Marketwired – April 26, 2016)

Riskalyze, the company that empowers thousands of advisors to align each client’s investments with their Risk Number®, today announced a unified solution to address the compliance implications of the Department of Labor’s (DOL) fiduciary rule. Nitrogen is stitching together its product line with updates, allowing advisors and firms to turn these industry challenges into opportunities.

Nitrogen representatives headlined this week at Tech Leaders (a Beacon Strategies conference) by addressing the implications of the DOL’s final rule. “No longer can advisors simply act in a client’s best interest,” said Kyle Van Pelt, Managing Director of Partnerships at Nitrogen, “Now they must be able to prove it.”

Advisors are already beginning to leverage the Risk Number® to demonstrate that they are acting in a client’s best interest. Nitrogen allows advisors to easily showcase alignment between portfolio construction and investor risk tolerance.

While the implementation of the Best Interest Contract Exemption (BICE) will be less cumbersome than originally feared, advisors will still need tools to manage the procurement of BICE forms. Nitrogen will automate the documentation a point-of-contact audit trail at each stage in the client relationship – from education, to investment recommendations, to client reviews.

Updates to Compliance Cloud will assist supervision teams in light of these new industry dynamics. Firms are now subject to increased legal exposure from breach-of-contract lawsuits when operating under one of several exemptions in the final rule. Compliance Cloud will empower teams to zero in on problems such as missing BICE documentation, mismatched risk objectives, high-risk positions, a high rate of 401(k) rollovers, or hyperactive accounts that may be abusing commission-based compensation.

Autopilot, Nitrogen’s digital advice platform, addresses an industry challenge presented by the DOL rule’s aversion to commission-based compensation. As a result to the rule, many firms will drop smaller, commission-based accounts because their perceived compliance risks outweigh their potential estimated revenue.

“Perhaps the greatest opportunity for advisors lies with the small accounts that will slip through the cracks,” said Aaron Klein, CEO at Nitrogen. “It may seem easier to abandon these accounts than to adapt them to the new regulations, but firms who can transition these smaller accounts onto a next-generation, fee-based digital advice platform will be able to take advantage of a unique opportunity.”

Advisors will leverage digital advice, married with automated asset management, to convert commission-based A-shares into fee-based accounts. The power of the Risk Number® on Autopilot will showcase best interest alignment and allow these accounts to be covered under the DOL’s fiduciary standard.

To provide a much needed resource to help advisors understand how the compliance landscape has changed, Nitrogen, in partnership with Beacon Strategies, has released a white paper titled, “No Need to Panic: A Roadmap to the DOL’s Final Fiduciary Rule and What It Means for Firms and Advisors.” Both firms have made the resource available for free at dol.riskalyze.com.

“Advisors and firms will have no time to procrastinate,” said Mike McDaniel, Chief Investment Officer at Nitrogen, “Implementation and enforcement of the DOL’s fiduciary rule will happen quickly. Firms who prepare themselves for DOL compliance will be the ones positioned to turn these industry challenges into opportunities.”

For media inquiries, please contact riskalyze@ficommpartners.com.

About Nitrogen

Nitrogen is the company that invented the Risk Number®, which powers the world’s first Risk Alignment Platform, empowers advisors to execute the digital advice business model with Autopilot, and enables compliance teams to spot issues, develop real-time visibility and navigate changing fiduciary rules with Compliance Cloud. Advisors, broker-dealers, RIAs, asset managers, custodians and clearing firms today manage $139 billion on Nitrogen’s platform in pursuit of its mission to align the world’s investments with each investor’s Risk Number. To learn more, visit www.riskalyze.com.

If there’s a common question that advisors raise when they first see Nitrogen, it’s this: why do you measure a client’s comfort zone and a portfolio’s 95% Historical Range using a six-month timeframe?

If there’s a common question that advisors raise when they first see Nitrogen, it’s this: why do you measure a client’s comfort zone and a portfolio’s 95% Historical Range using a six-month timeframe?Let’s tackle a few of the most common questions and fears about the six-month range.

A: If you use the 95% Historical Range to promise performance — something no advisor should do! — that might be a problem. But the idea is to use the analytic to give the client some semblance of what “normal” is for the portfolio you’ve built for them, and set expectations you can consistently achieve.

“As you know, there is about 5% of the risk that we can’t quantify for you, the ‘black swan’ type events we saw in 2008 are a good example. My job as your advisor is to control the 95% of the risk that we can quantify. So, six months from now, we’ll take a look at your portfolio, and if it’s anywhere between X% and Y%, that would be totally normal for this portfolio.”

A: Nitrogen incorporates decades of behavioral economics research, and everything we’ve seen and experienced ourselves has confirmed that one year is just too long for a client to “hang in there” if they are in the midst of volatile markets and worried about their downside risk. These clients need a shorter timeframe than one year to keep them invested for the long term.

A: It is said that a journey of a thousand miles begins with one step, but it’s also true that nobody invests for twenty years towards retirement. Psychologically, your clients are investing for a large number of much shorter time periods. And the short-term decisions they make along the way will have a profound long-term impact.

Put another way, one cannot travel to a destination without knowing where they are starting from, and how they’re going to get there. What good is an itinerary from Los Angeles to New York without the knowledge that the traveler is psychologically unable to board an airplane?

Far too many advisors respond to that kind of client by effectively saying “look, everybody flies and you’ll just need to get on the plane.” Effective advisors are able to show the client their tradeoffs. Traveling to New York by train is possible; it’ll just take a lot longer to get there. Or perhaps the client can proactively accept more risk than they wanted. Either way, you’ve now created invaluable alignment between you, your client and their portfolio.

As one advisor put it recently, “Nitrogen informs today’s decisions within the context of a long-term plan.” Join the movement and turn your clients into fearless investors — we’d love to help.

Today at T3 our CEO Aaron Klein unveiled a game-changing behavioral coaching solution for advisors of all stripes. Read the full release below.

Nitrogen Introduces ‘Check-ins’, Automated Behavioral Coaching Tools for Advisors

• New analytics help the advisor put markets, portfolios and risk in context for clients during semi-annual client reviews.

• Monthly check-ins build a strong foundation to support the advisor’s message between client reviews and give advisors an early warning signal when client psychology is deteriorating.

• The constant fight by advisors to keep client psychology positive becomes remarkably easier with the consistent support of Check-ins and these powerful new analytics.

Sacramento, CA – February 10, 2016 – Nitrogen, the company that has equipped thousands of advisors with the Risk Number™, today announced powerful new tools that revolutionize the ability of advisors to put the markets in context for their clients during client reviews, support client psychology between those reviews, and deliver consistent behavioral coaching that promotes long-term investing.

Nitrogen CEO Aaron Klein unveiled these features at the Technology Tools for Today (T3) Conference in Fort Lauderdale, Florida this morning.

Advisors have used Nitrogen for a long time to effectively set risk expectations for client portfolios, but with Client Analytics, the conversation shifts to demonstrating how well the Risk Number was able to meet those expectations and compare the outcome to the advisor’s choice of benchmark. The result is a powerful way to give the client context for why market volatility is “normal” and help clients stay the course when they may be concerned and prone to knee-jerk reactions.

Advisors can leverage a powerful ally in supporting client psychology in between those reviews by enabling Check-ins, a monthly email that gathers two simple data points from each client, and proactively supports the advisor’s message with adaptive analytics that fit the context of the markets.

Two simple questions mark each client’s check-in — “how are you feeling about the markets?” and “how are you feeling about your financial future?” With two taps on their smartphone, clients see adaptive analytics that help them understand what is “normal” for their portfolio, and advisors get an early warning system when a client relationship needs care.

“It has been well-documented that 4 out of 5 clients who leave an advisor do so because of communication failures,” said Aaron Klein, CEO at Nitrogen. “The most successful advisors are the ones who view their job as behavioral coach, helping clients make the right decisions even in times of fear. Client Analytics and Check-ins are powerful tools to help advisors deliver that coaching consistently and effectively.”

“Let’s remember what we’ve learned with the Risk Number — clients are individuals,” said Mike McDaniel, Chief Investment Officer at Nitrogen. “Check-ins give advisors the ability to leverage their time, support the client’s psychology and capture the state of each client’s unique outlook and concerns in real-time.”

Check-ins and Client Analytics will go live for every Nitrogen customer in May. Both features will be a free upgrade for existing customers on Solo, Team or Enterprise plans.

# # #

For media inquiries regarding Nitrogen, please contact riskalyze@ficommpartners.com.

About Nitrogen

Nitrogen is the company that invented the Risk Number™, which powers the world’s first Risk Alignment Platform, empowers advisors to execute the digital advice business model with Autopilot, and enables compliance teams to spot issues, develop real-time visibility and navigate changing fiduciary rules with Compliance Cloud. Advisors, broker-dealers, RIAs, asset managers, custodians and clearing firms today manage $121 billion on Nitrogen’s platform in pursuit of its mission to align the world’s investments with each investor’s Risk Number. To learn more, visit www.riskalyze.com.