As a product manager at Nitrogen, I get to talk to advisors on a regular basis – discussing their day-to-day work processes, how they interact with their clients, and the problems that Nitrogen can solve for them through technology. Central to all of these conversations is the Risk Number, and what that simple expression of risk tolerance and alignment has done to transform the advisor-client relationship.

Advisors tell me all the time how the Risk Number facilitates a simpler conversation around market volatility and the tradeoff between risk and reward.

Simply put, everyone just gets the Risk Number. From the “highly-detailed” client who writes love letters to standard deviations, to the clients who pay an advisor so they never have to look at a number again – everyone has a Risk Number and everyone understands it.

I’m proud to be a part of the team that has changed the way advisors talk with their clients, but the Risk Number isn’t all we do! There are hundreds of features in our platform (seriously – you should see our product inventory!) and today I’ll highlight a few of my favorite conversation starters – Stress Tests, Retirement Maps, and Stats.

Stress Tests

No matter how much you steer a client toward staying invested within their comfort zone so they can meet their long-term goals, people have a natural inclination for that “grass is greener” mentality. They watch the news. They talk to their neighbor. They know how the market is performing, and from there, it’s an easy jump to that age-old question: “Why is the market beating my portfolio?”

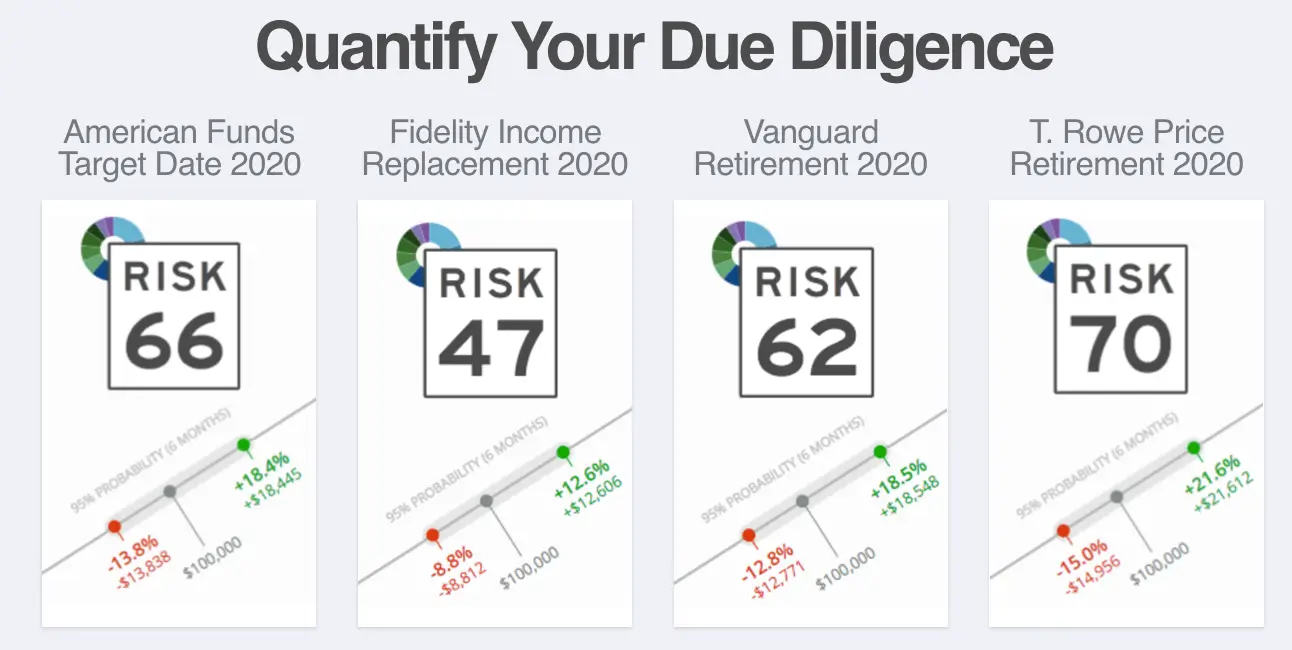

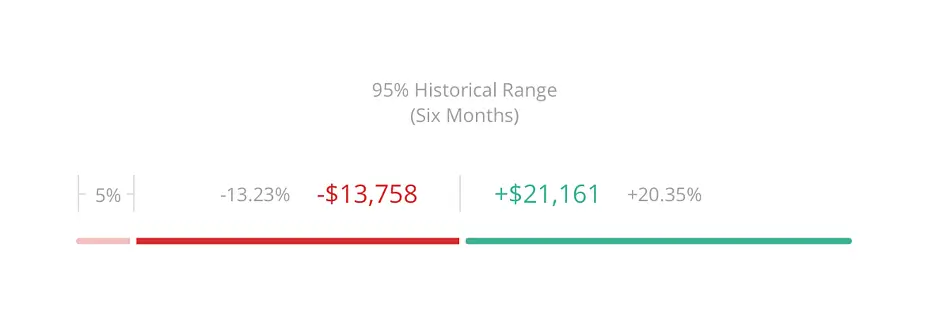

With Stress Tests, we’ve empowered advisors to answer that question – to have that conversation – with the click of a button. Everyone wants more returns and higher ceilings on their investments, but we invest within our risk tolerance because not everyone is comfortable with the potential downside that comes with aiming for that additional return. Stress Tests equip advisors with a simple, visual presentation of this concept – expressed through the lens of historical market scenarios.

This naturally facilitates some very crucial talking points around the differences between, say, a 50 portfolio and an 85 portfolio. In an up market like 2013, that 85 portfolio is likely to beat the 50 by a wide margin, but if a market similar to the one we saw in 2008 were to occur, that same 85 would lose much more than a Risk Number 50 client may be comfortable with. We’ve selected four historical market scenarios to display by default within the Stress Tests view, but you can easily hide the ones you don’t want or put on your “power user” hat and display any custom Scenarios you’ve saved. Not sure how? Check out our KB articles on Stress Tests and Scenarios or schedule a call with one of our awesome coaches to learn more!

Retirement Maps

After you’ve determined how much risk a client is comfortable with, and how much risk they have in their current investments, the next step is to determine how much risk they need in order to meet their long-term goals. Here’s where Retirement Maps step in.

While there is tremendous value in developing a detailed financial plan, Retirement Maps allow the advisor to keep the conversation around retirement lightweight. With just a few simple inputs (initial investment, monthly savings, retirement date, and monthly withdrawal after retirement) we’ll determine how likely a client is to retire with the amount of money they need. If you’ve already developed a proposal for this client, you can easily flip between their current investments and your proposal for their portfolio to illustrate the differences. I just love how simple this chart is. Give us four basic inputs and we’ll do all the hard math, allowing you to focus on the client. By no means is this meant to be an exhaustive result, but it’s a great tool for advisors to reorient a client toward a long-term mindset. I love it for these scenarios as well:

Demonstrate to someone with high risk tolerance why they don’t need to expose themselves to all that risk in order to meet their retirement goal.

Reassure an uneasy client that six months of volatility is well within expectations for their portfolio.

Help clients see that you can have volatility and still hit your goals.

Our Retirement Maps are so effective at making these conversations productive. Make sure your client sees that green retirement probability every time they’re in your office.

Stats

Stats is such an interesting case because we delayed building out a more robust analytics module for a long time. We were focused on innovating the advisor-client engagement process and keeping all that math under the hood. Month after month, though, this remained our most requested feature by advisors – particularly advisors who love building portfolios in Nitrogen.

We shipped Stats for Nitrogen Premier back in June, and it includes a ton of useful analysis for advisors, surfacing interactive performance illustrations, dynamic analytics tables, visual correlation analysis, sector and region breakdowns, and much more. So much of our focus here went into the visuals. We wanted to create a platform for analysis that provided value to the advisor, but was presentable and approachable in a way so many analytics tools aren’t.

What we’ve heard from the advisors using Stats is one of the reasons I love working in product. Powerful visuals promote powerful conversations, and we’ve seen this with Stats over and over again. Not only are advisors using Stats when building out portfolios, they’re also using it in meetings with their more analytically-inclined clients.

With Stats, it’s easier than ever to illustrate a client portfolio’s performance in line with its benchmark, while surfacing some meaningful statistics for the time frame you select. Whether or not you choose to explain Sharpe Ratios, the presentational aspect of Stats works well with clients to reassure them of all the considerations that go into building their portfolio, while also providing you with some useful talking points on portfolio composition.

If you’re one of the many advisors already taking advantage of Stats, all I can say for now is “stay tuned.” The response has been so positive, and we’re just getting started!

Having a role in building products at Nitrogen is truly a privilege. What I’ve found is that for every feature we build, there are thousands of conversations we facilitate. Thank you for having those conversations with your clients and helping us to empower the world to invest fearlessly.