Some of the most important moments in an advisor-client relationship happen when something complicated suddenly becomes clear.

A prospect sees the risk in their current portfolio. A client understands how their income plan could work in retirement. A tax conversation turns into a planning opportunity. A family starts thinking more intentionally about what happens when wealth transfers.

At Nitrogen, we call these Catalyst Moments.

This spring, we’re expanding what those moments can look like.

Our latest product launch introduces Legacy Center, a new product designed to help advisors build intentional relationships with beneficiaries before wealth transfers.

We’re also rolling out major updates across all of our products, including more connected AI workflows, deeper planning capabilities, and new client-ready visuals.

Meet Legacy Center

Advisors spend years helping clients build, manage, and protect wealth. But when that wealth eventually transfers, the next generation often has no relationship with the advisor who helped build the plan.

Beneficiaries may choose someone they already know. Families may avoid talking openly about estate details. And advisors may not have a natural way to introduce themselves without the conversation feeling awkward or poorly timed.

Legacy Center is designed to turn that into a natural moment.

We surveyed 345 advisors and found that 98% believe the generational wealth transfer will significantly impact their business, yet only 42% say they have a working plan to address it.

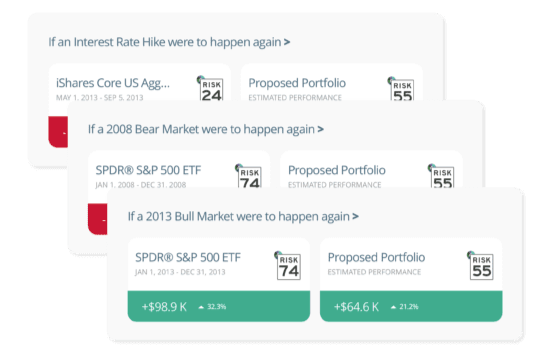

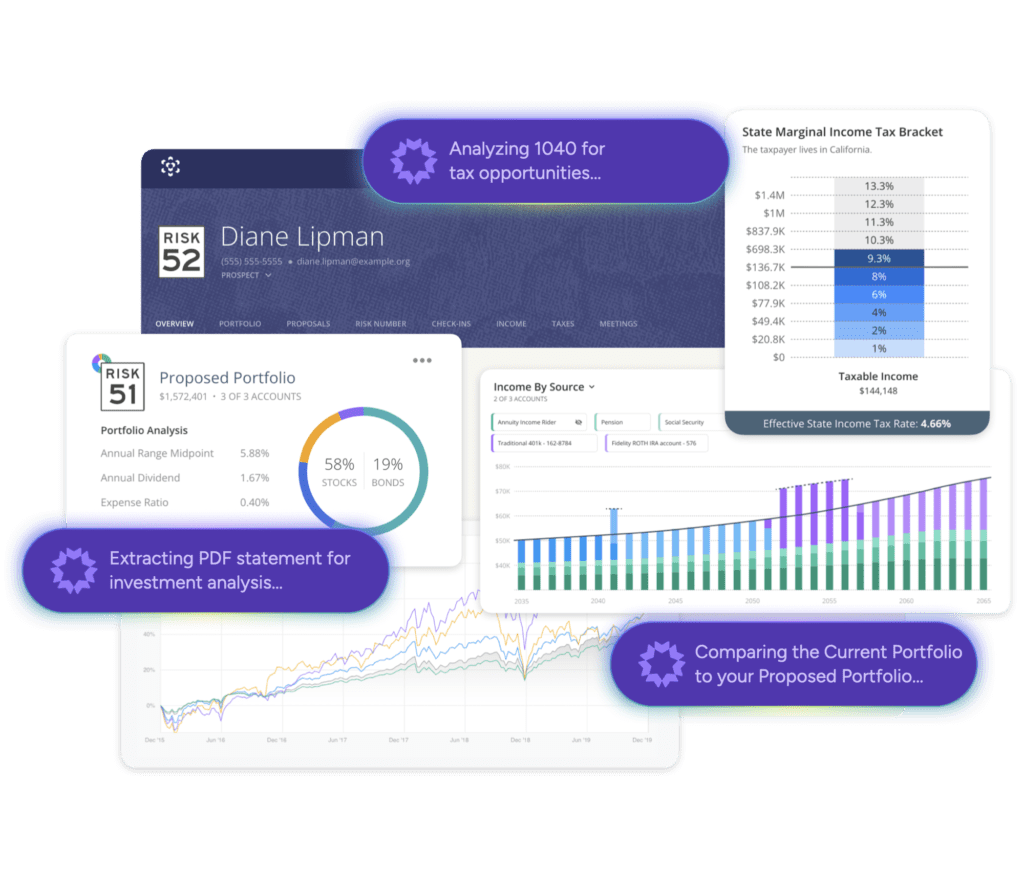

With Legacy Center, advisors can illustrate a client’s projected estate, add beneficiaries, and assign trusts while showing how assets may transfer over time. Instead of discussing percentages on a document, advisors can help clients visualize the real future impact of their plan.

A client can see what each child, grandchild, or organization may receive. They can understand how their legacy may support the people and causes they care about. And from there, advisors can create prospective client profiles for beneficiaries who may need guidance in the future.

Legacy Center also introduces Legacy Key. These are formal, branded introductions advisors can send to beneficiaries with the client’s permission. They give the next generation a clear point of contact and a natural reason to connect when the time comes.

Legacy Center is available now. Legacy Keys will become available next month.

Nucleus Expands Across the Advisor Workflow

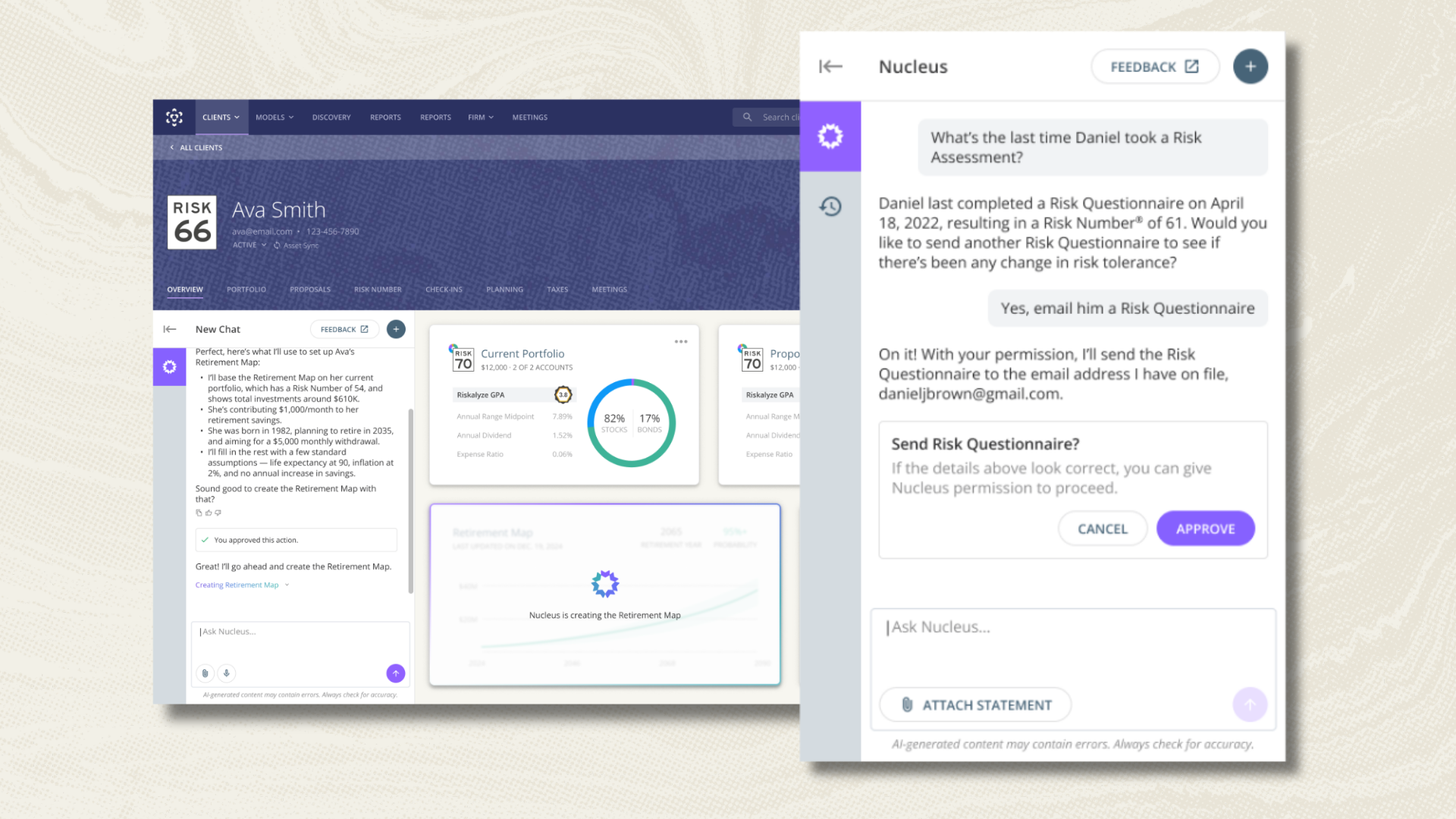

When we introduced Nucleus earlier this year, the goal was simple: build an AI agent that could help advisors take action, not just generate answers.

This spring, Nucleus became more deeply connected across the Nitrogen suite.

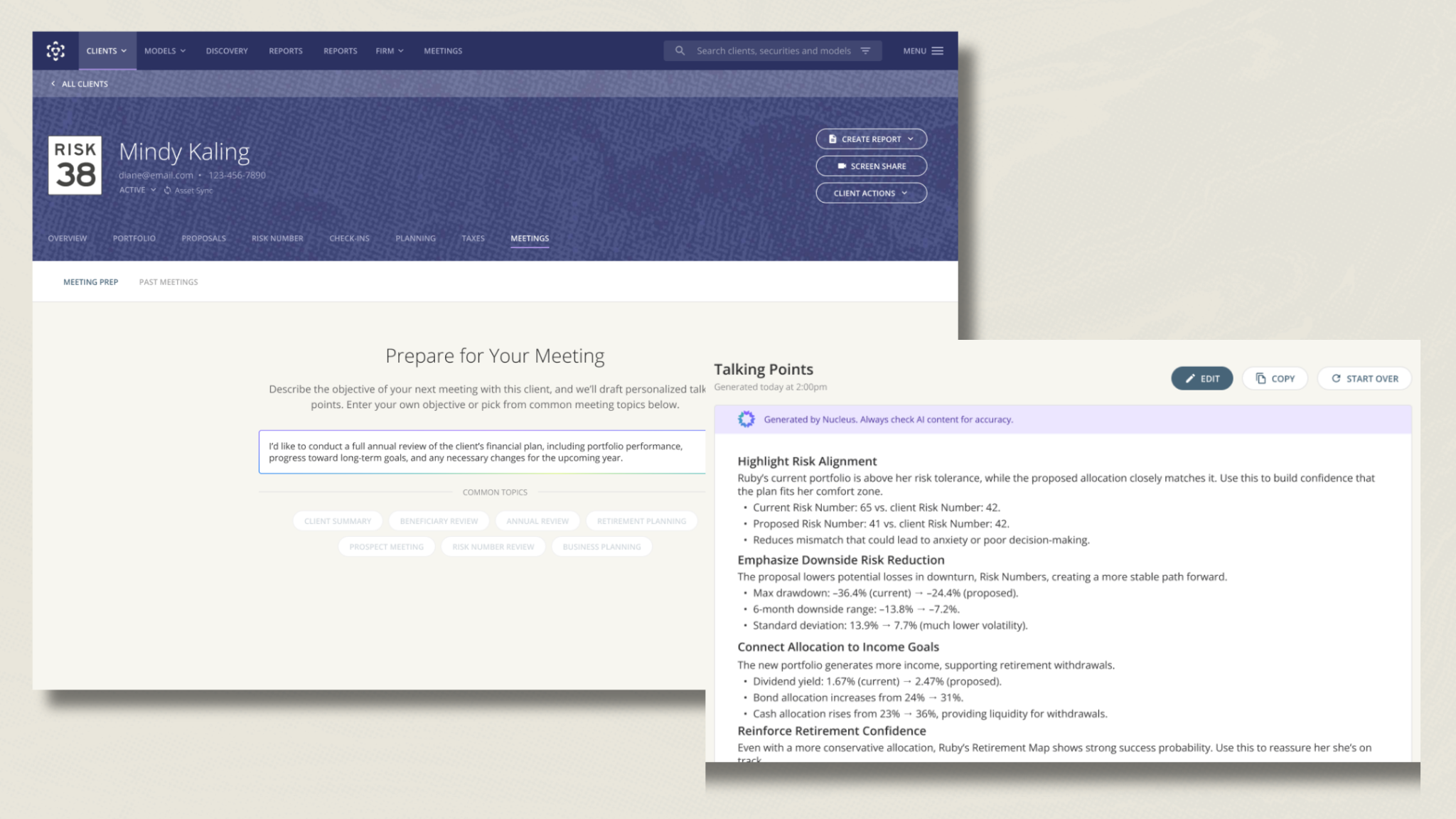

Advisors can now use Nucleus across more workflows, including turning investment statements into portfolios, preparing for meetings, generating Retirement Maps, surfacing Research Center analytics, and searching CRM data. Nucleus also now stays context-aware across client tabs, allowing advisors to continue workflows without restarting the conversation each time they navigate the platform.

The launch also introduces deeper Research Center connectivity, native Wealthbox support, and expanded CRM search capabilities. For firms that rely heavily on CRM workflows, Nucleus can now help surface client notes and account details faster.

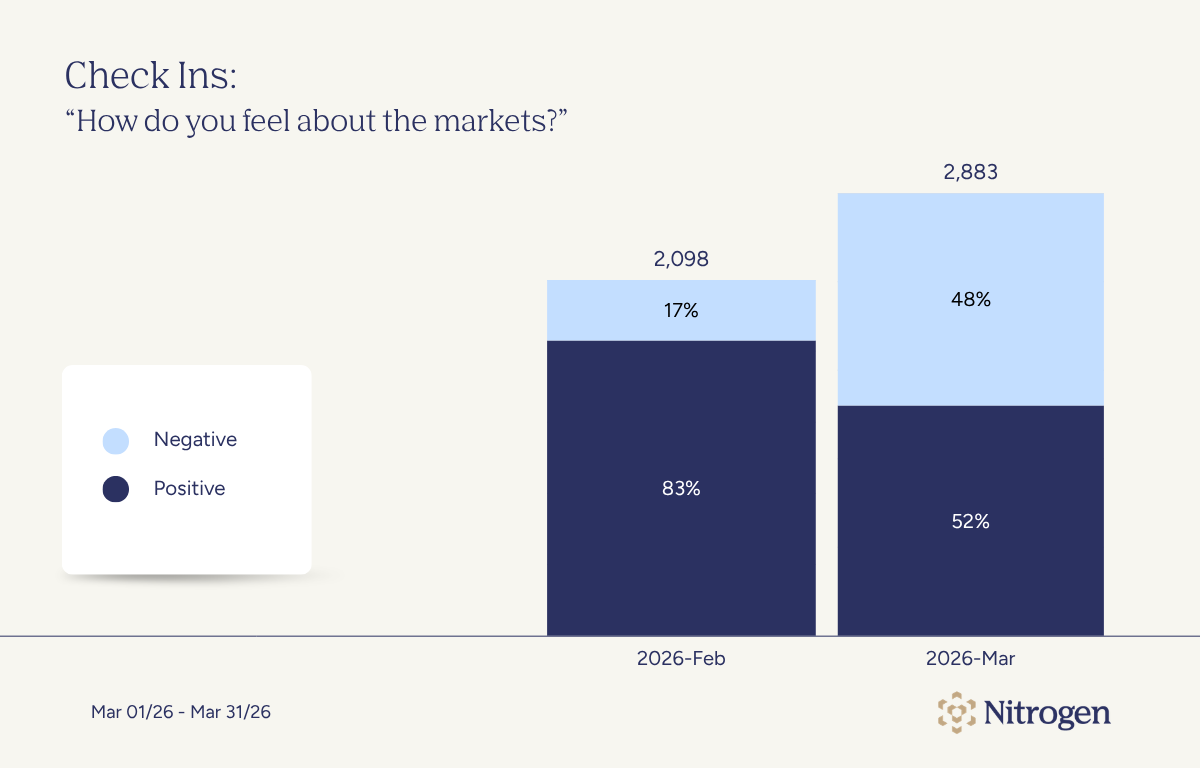

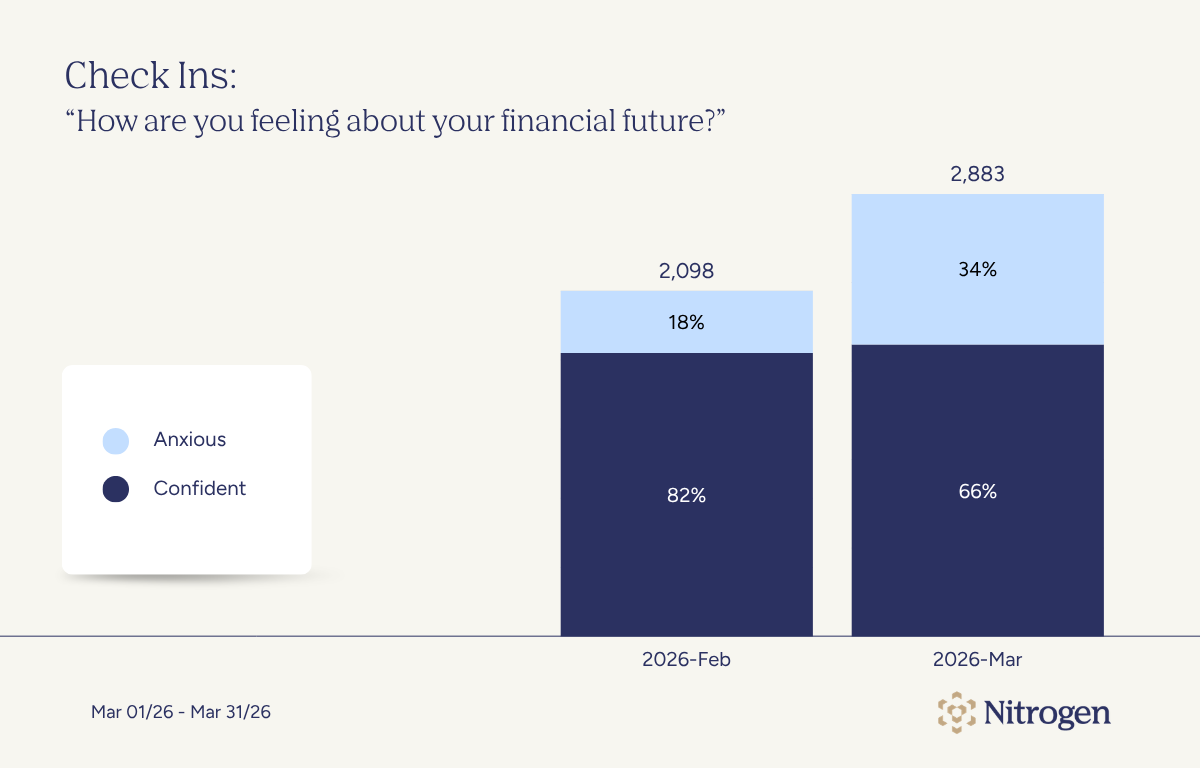

More Proactive Planning Conversations

Tax and retirement planning are full of moving pieces. Clients may understand the broad idea, but they usually need help seeing the tradeoffs clearly.

This release adds several new tools designed to make those conversations easier.

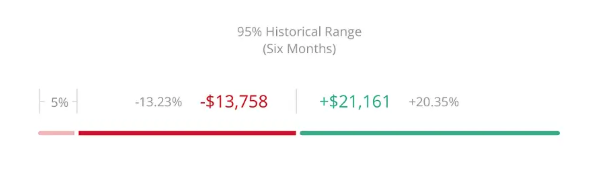

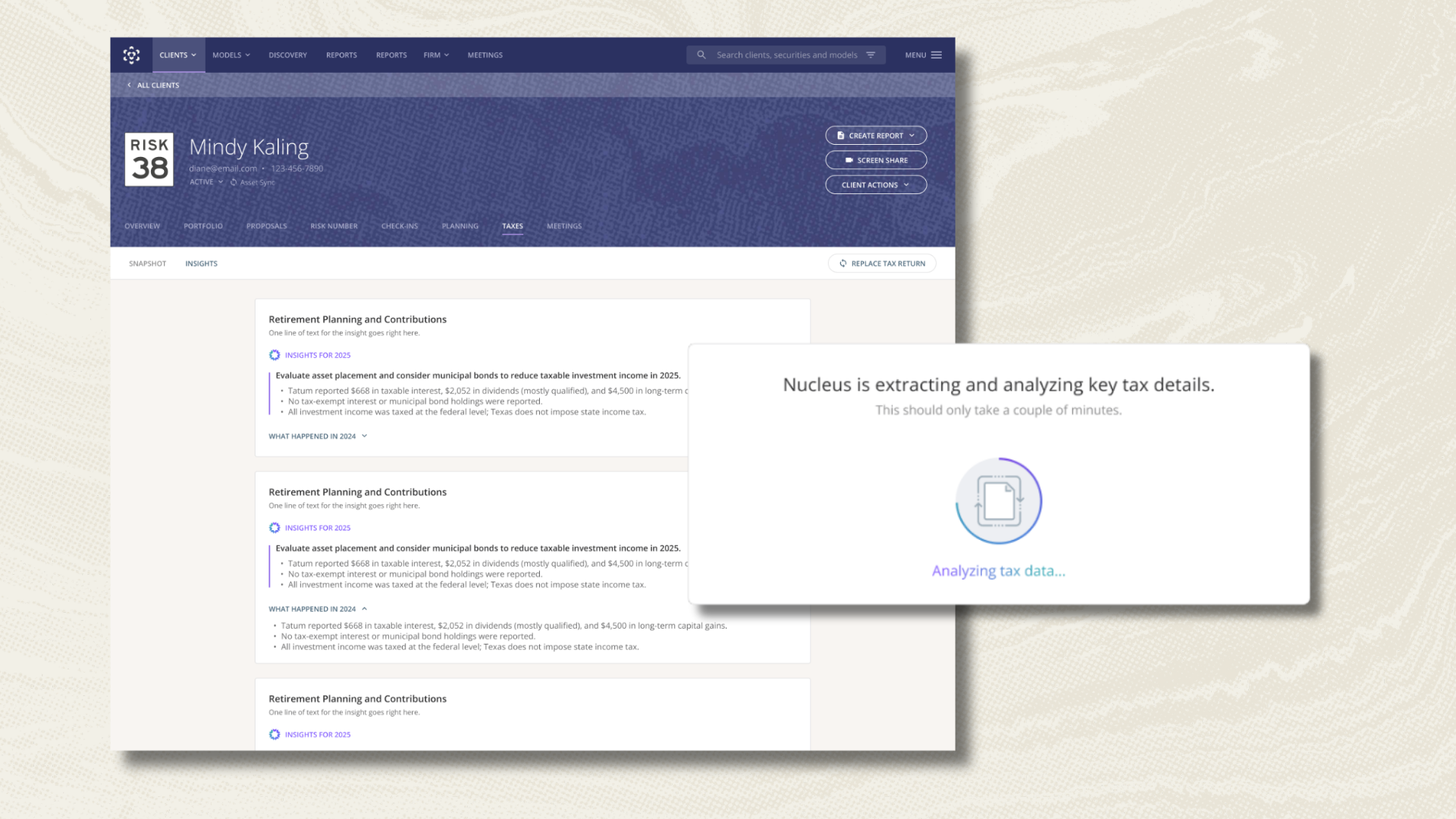

In Tax Center, the new Roth Conversion Calculator helps advisors show the impact of a potential Roth conversion using client-specific data. Advisors can model a lump-sum conversion or multi-year strategy, then show the estimated cost today, potential savings in retirement, and the break-even point.

It also includes a death benefit comparison, helping clients see how a Roth conversion may affect what beneficiaries inherit after taxes.

Tax Center also adds Tax Scenarios. Advisors can now model “what if” questions in real time, such as a change in filing status, additional income or more capital gains. The Tax Snapshot recalculates with clear before-and-after comparisons, helping clients understand how a life event or planning decision may change their tax picture.

Finally, Income Center also gets a new account balance view. Advisors can show how account balances may change over time, helping clients understand drawdown order across different accounts. For example, a client can see why it may be okay for one account to decline first if another account continues growing before it’s needed.

Together, these updates make planning conversations more visual, more specific, and more proactive.

Tax Center is also now included in Nitrogen Complete at no additional cost.

More Updates to Help Advisors Move Faster

This launch also includes several updates designed to remove everyday workflow friction.

In Risk Center, advisors can now associate models with fact sheets, so the right materials are automatically included in Reports Builder. Models subscribed to through the Partner Store can also auto-update when providers publish new versions.

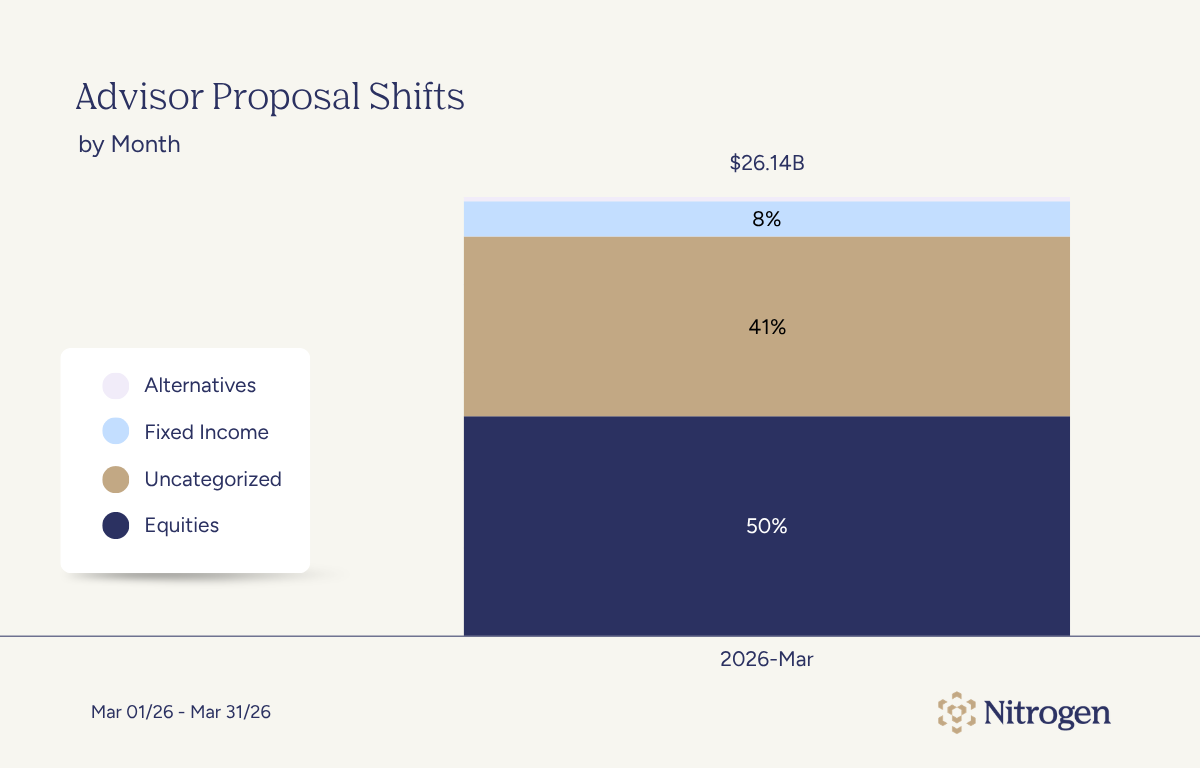

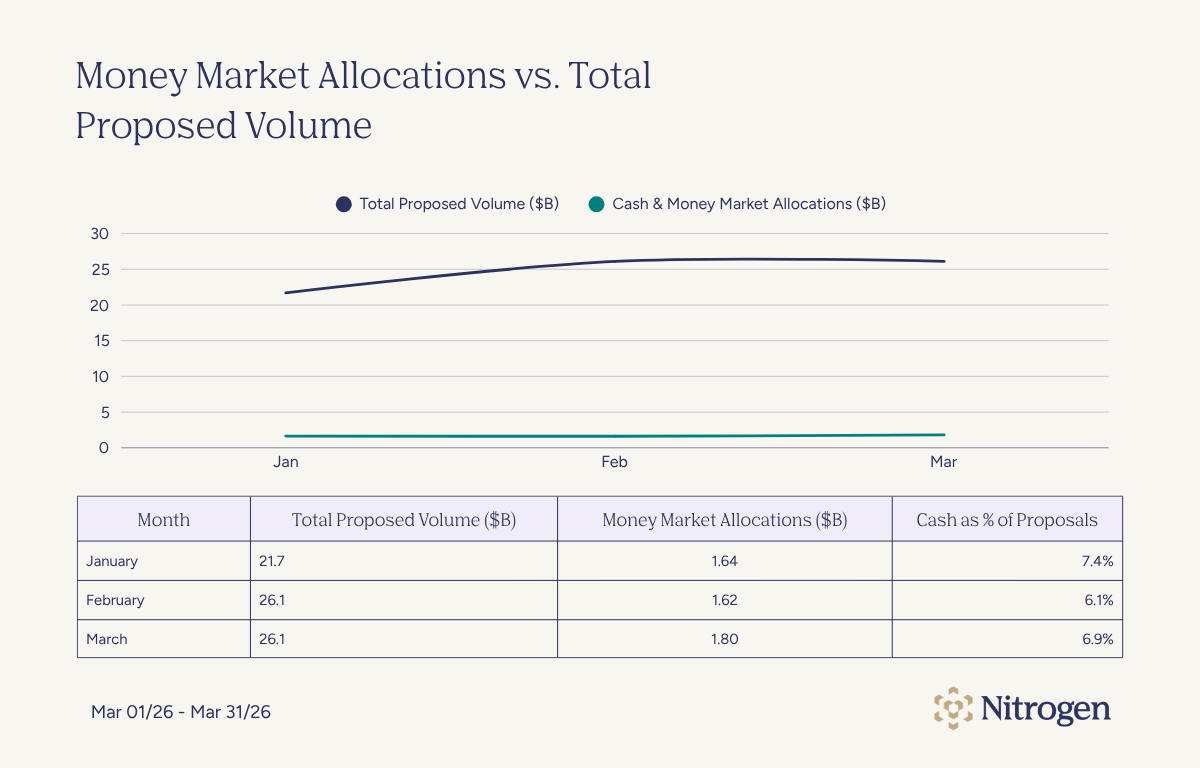

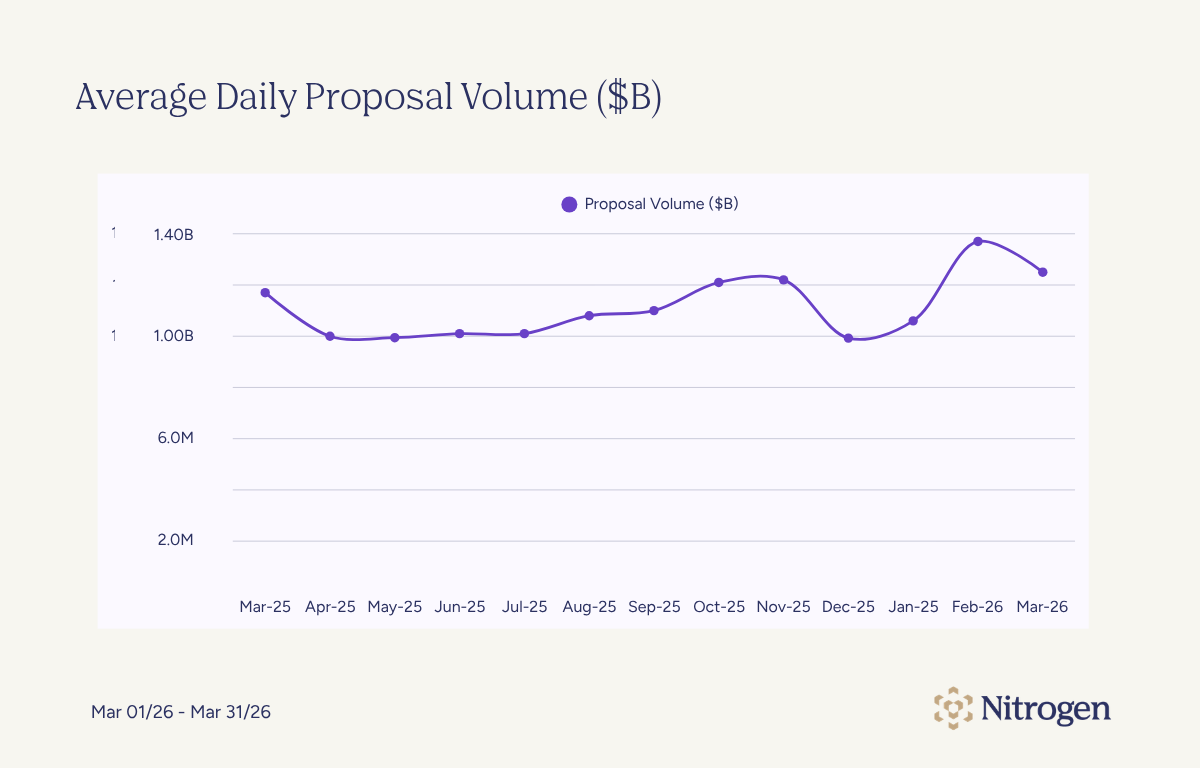

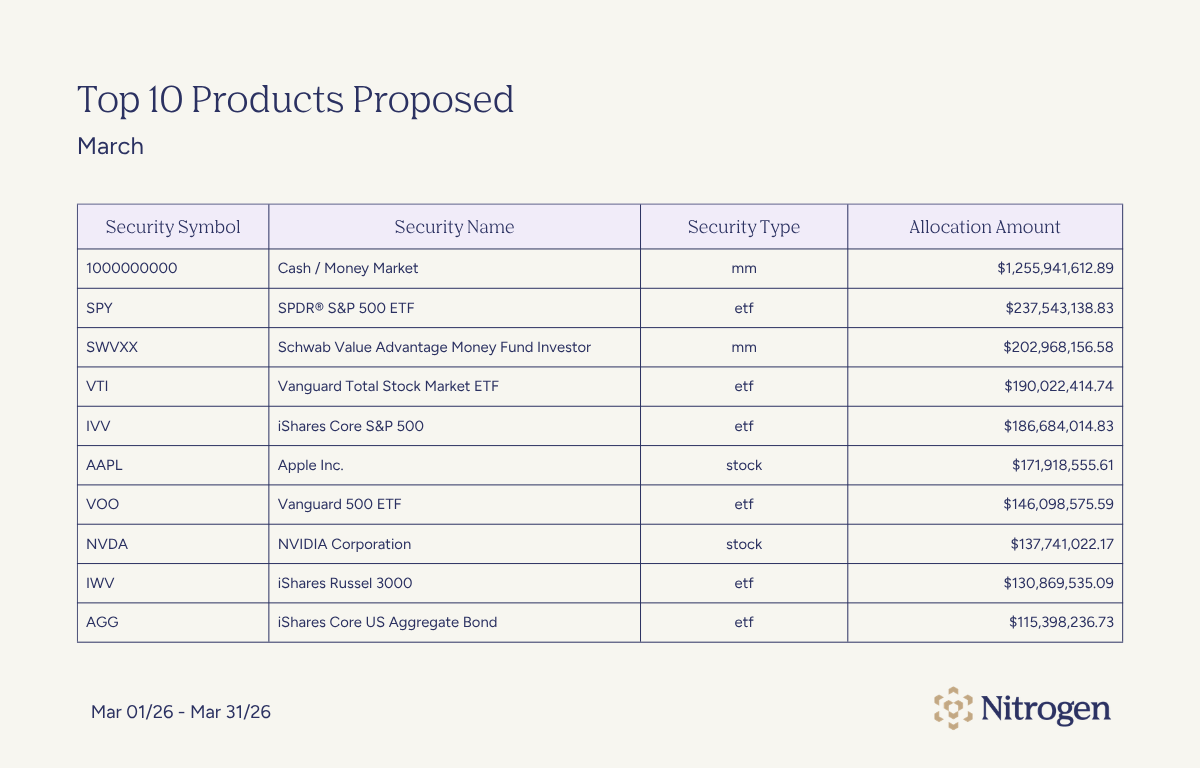

Money market funds are now first-class assets in Nitrogen, with improved discovery, modeling, and tax treatment. Variable annuity groupings also stay fresher through additional automation when insurers rename or restructure products.

Research Center is also getting faster and more flexible too, with support for larger portfolios in Modeled Performance, faster load times, expanded Discovery filters, and smarter search rankings.

More Included with Nitrogen Complete

With this launch, Nitrogen Complete now includes both Tax Center and Legacy Center.

That means advisors on Complete now have access to Risk Center, Income Center, Research Center, Tax Center, and Legacy Center, all powered by Nucleus.

For firms that want a more connected planning experience, Complete now covers more of the advisor-client relationship, from risk and investments to income, taxes, and legacy planning.

Create More Catalyst Moments with Nitrogen

Every update in this spring launch is designed around the same idea: helping advisors create more Catalyst Moments.

Whether that’s helping a client better understand their risk, visualize their retirement income, navigate a tax decision or start planning for the next generation, these moments are where stronger client relationships are built.

To explore the new features in more detail, book a demo with the Nitrogen team or watch the replay of our Spring Product Launch event.

FAQ

What is Legacy Center?

Legacy Center is Nitrogen’s product for helping advisors build intentional relationships with their clients’ beneficiaries before a wealth transfer occurs. Using data already in Nitrogen, advisors can generate a Legacy Map, a visual picture of a client’s full projected estate, including accounts, trusts, insurance policies, and beneficiaries tied to real projected dollar amounts. From there, advisors can create prospective client profiles for beneficiaries and send Legacy Keys: formal, advisor-branded introductions that give the next generation a clear point of contact for when the time comes.

What is a Legacy Key?

A Legacy Key is a formal, branded introduction advisors can send directly to a client’s beneficiaries through Nitrogen, with the client’s permission. It gives beneficiaries the right contact information and enough context that when the time comes, they know exactly who to reach out to and why their family trusted that advisor. Legacy Keys are designed to earn a spot in the keep folder. Legacy Map is available today. Legacy Keys begin rolling out in June 2026.

What is the Great Wealth Transfer?

An estimated $84 trillion in assets is expected to pass from one generation to the next over the coming decades. For financial advisors, that creates both a significant risk and a meaningful opportunity. When a client passes, assets tend to follow existing relationships, and most beneficiaries don’t have one with their parent’s advisor. We surveyed 345 advisors and found that 98% believe the generational wealth transfer will significantly impact their business, yet only 42% say they have a working plan to address it. Legacy Center is designed to help advisors start building those next-gen relationships now, before a transfer happens.

Is Legacy Center included in Nitrogen Complete?

Yes. Legacy Center is now included in Nitrogen Complete at no additional cost. With this launch, Complete bundles all five advisor products: Risk Center, Income Center, Research Center, Tax Center, and Legacy Center all powered by Nucleus.

Is Tax Center included in Nitrogen Complete?

Yes. As of today, Tax Center is also included in Nitrogen Complete at no additional cost.

When will Legacy Keys become available?

Legacy Center is available now. Legacy Keys, which allow advisors to send formal, branded introductions to beneficiaries, will become available next month (June 2026).

What is Nucleus?

Nucleus is Nitrogen’s agentic AI engine. Unlike a standard AI chatbot, Nucleus doesn’t just generate answers, it takes action. It can turn investment statements into portfolios, prepare meeting briefs, generate Retirement Maps, surface Research Center analytics, and search CRM data, all from a single conversation. Nucleus stays context-aware as advisors move between client tabs, so there’s no need to restart a workflow mid-conversation. Since launching in February 2026, Nucleus has surpassed 10,000 advisors and powers every product in the Nitrogen suite.